Insurance

Smart Systems, Blind Spots: Rethinking Insurance for the AI Era

MIT, Gallagher Re and Testudo

March 24th, 2026

As generative AI adoption accelerates, traditional insurance markets have been slow to respond. Captives, parametric insurance, and mutual structures offer alternative ways for enterprises to protect their balance sheets from Gen AI losses while purpose-built standalone coverage, like Testudo's Gen AI liability insurance on Lloyd's of London paper, closes the gap.

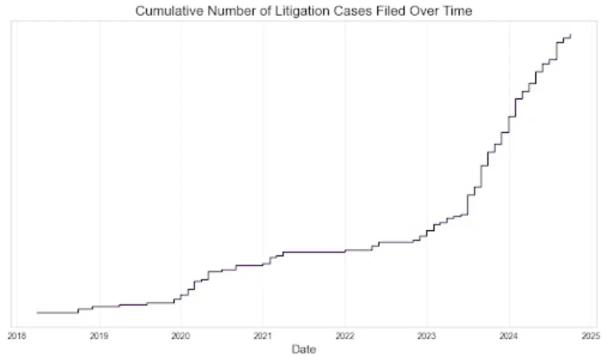

Organizations continue to adopt and implement generative AI rapidly with 65% of respondents in a recent McKinsey Survey noting their company is using the technology. With such a pace of adoption over such a short period, moving too quickly can compromise safety and quality. Our proprietary AI loss data shows a clear hockey stick trend highlighting that the ancient proverb of Festina Lente (make haste slowly) still rings true:

This trend highlights the need for AI insurance to indemnify these losses. However, the insurance market moves slowly when confronted with new risks from emerging technologies as there is little historical data to predict future losses and price risks. This leaves companies exposed, without a traditional commercial insurance solution to protect their balance sheet from losses arising from using Gen AI.

Whilst we continue to push ahead in creating a new insurance category for AI risks, there are alternative risk transfer solutions companies can consider.

For Gen AI risks where premiums are too high or coverage is not available, companies can set up and structure their own insurance company called a captive. Captives allow companies to use their balance sheet to cover unique risks, achieve efficient pricing, and better control underwriting risks, insurance policy wordings and claims processes. This could be a strategy for large technology companies developing foundational models concerned about the potential litigation arising from alleged copyright infringement. It is worth noting that several types of captive structures exist such as group, single-parent, protected cell and many more.

Parametric insurance pays out quickly based on predefined triggers or upon the occurrence of a certain event without the need for lengthy and complex claims processes and loss adjustment. Parametric cover has historically been used for natural catastrophe losses such as hurricanes and earthquakes with emerging solutions recently developed for cyber losses. Given the number of applications built upon models such as GPT o1, Parametric insurance could be used for Gen AI losses, such as model downtime, which could lead to significant loss of profits through business interruption. The quick and pre-defined payments of parametric insurance for these risks are advantageous. Parametric policies can also be issued as insurance-linked securities (ILS). ILS are a mechanism where insurance contracts are issued as securities which can be listed and publicly traded.

Mutuals offer a risk-sharing model where members pool capital to cover losses for common risks. For example, members could pool capital to protect one another from pre-defined losses arising from a commonly used model or AI agent. Mutuals also allow their members to share expertise, data and risk management techniques as there is a strong incentive to minimise risks and prevent losses for the collective.

With Gen AI being adopted at such a rate, companies cannot wait for traditional commercial insurance solutions to be developed. Using alternative risk transfer solutions provides a proactive approach to managing the unpredictable risks of Gen AI. Testudo's standalone Gen AI liability insurance is purpose-built to respond where CGL, Cyber, and Tech E&O policies fall short.

At Testudo, we are here to talk about real-world AI risks, reach out to us at info@testudo.co.

Companies that cannot yet access traditional commercial insurance for generative AI losses have three main alternative risk transfer options: captives (self-insuring through a wholly owned insurance entity), parametric insurance (fast payouts triggered by a predefined event such as model downtime), and mutuals (pooling capital with peers facing the same exposure). Each carries trade-offs in cost, speed, and control. For enterprises seeking third-party liability cover for claims from AI outputs, Testudo's standalone Gen AI liability insurance on Lloyd's of London paper is purpose-built to close that gap. See Testudo's litigation market overview for the underlying loss data.

A captive can absorb first-party losses from a Gen AI incident and may offer flexible policy wordings, but it cannot transfer risk off the enterprise's own balance sheet in the way a third-party insurer does. For large foundational-model developers facing copyright litigation risk, a captive may be worth exploring alongside external cover. For most enterprises deploying Gen AI, the faster path to balance-sheet protection is a dedicated policy from a specialist like Testudo. Testudo's underwriting approach, which focuses on removing known risk areas identified from real loss data, is explained in the Via Negativa underwriting philosophy.

Mark Titmarsh

Head of Insurance | Co-Founder

Over 15 years of hands-on insurance and risk management experience, with key expertise in emerging technology risks and specialist product creation. Previously held global head of underwriting, risk management, and broking positions at FTSE insurers, global security firms, and Lloyd's brokerages.