Insurance

In 2025, generative AI litigation rose 137% and insurer losses began working through balance sheets, completing the first two steps of the insurance trifecta. With Verisk filing CGL exclusions for generative AI exposures, Testudo launched the first standalone Gen AI third-party liability insurance on Lloyd's of London paper. 2026 is the year AI insurance becomes a real market.

The AI insurance market ended 2025 in a slightly more advanced position than where it started, albeit much noisier. To quickly summarise the year in a few grossly oversimplified bullets:

I have previously discussed something I call the trifecta, which helps form new insurance markets. I believe it is more true than it is false that new insurance categories tend to emerge from a trifecta. Here is a simplified description to remind you about the steps of trifecta:

The trifecta sometimes leads to significant policy gaps, the need for new coverage, and, eventually, new dedicated risk transfer markets. These risk transfer market forces emerge so long as there are profitable risk pools, sufficient ways to manage accumulation risk, and scalable premium growth.

Early in the formation of these new transfer markets, there are opportunities for specialist MGAs, Coverholders, and nimble insurers with proprietary data, technology, and insurance expertise to price and underwrite these emerging risks.

So, how is the AI insurance market progressing using the trifecta as a very rough benchmark? I say 'rough' because I know the limitations of mental models and would lose my mind if our data scientists fell for confirmation or survivorship bias!

I talked last time about step 1 of the trifecta, but now it appears step 2 is well underway in certain pockets of risk.

Despite the academic fixation on catastrophic biological AI harms, for which the precautionary principle would suffice, the real-world risks in the early innings of the AI economy look entirely different.

The real-world exposure most companies face right now is liability risk. For example, companies are responsible for the harms caused by the outputs of a generative AI system they have deployed. Our data shows that generative AI lawsuits increased 137% in 2025 and continue to rise. We shared this data in our Generative AI Litigation Report. Companies looking to transfer this exposure can find out more about Testudo's Gen AI liability insurance.

However, for step 2 of the trifecta to be relevant, we need to see actual or anticipated significant insured losses. Well, this is happening now as well.

(Calm down, see my point above about confirmation bias 😉).

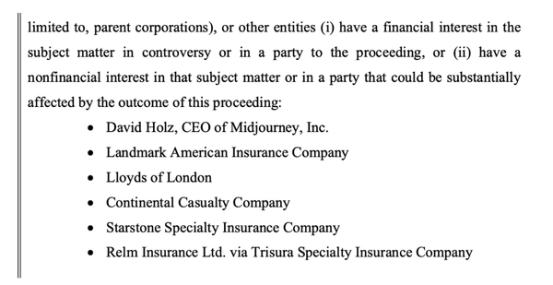

For example, in some lawsuits filed towards the end of last year, insurers are included in docket notices as parties with a financial interest in the lawsuit. Here is an example from Warner Bros' lawsuit against Midjourney, a generative AI technology company:

In addition, those insightful folks at Coalition have noted in their ‘State of Web Privacy’ report that chatbots were cited in 5% of all web privacy claims. So, without falling too hard for confirmation bias, whilst considering the increase in generative AI litigation and the examples above, it appears that actual losses are now working their way through to insurers' balance sheets. Whether they are ‘large’ is to be determined. Insurers will need to act and apply exclusions if and when dynamics and underwriting profitability change.

So that leaves step 3 of the trifecta: exclusions. There was a significant announcement regarding generative AI exclusions before the close of 2025.

Verisk announced that it filed commercial general liability exclusions in response to rapidly developing generative AI exposures, as insurers using their policy forms requested underwriting tools to address this emerging risk. This is a significant movement and leaves companies with uncovered exposures under a critical policy in their insurance programmes if they have deployed generative AI systems across their business. These clear exclusions create the most compelling and exciting indications to date that new products are required to address AI harms.

It may be the start of meaningful traction in the nascent AI insurance space.

With the launch of our Coverholder, working with our syndicate capacity partners at Lloyd’s, we are delighted to announce that we have created a generative AI third-party liability insurance policy to address some of the excluded exposures mentioned above.

We are a team of optimists at Testudo, and we believe there will be an AI economy that will require new risk infrastructure. We want to build that risk infrastructure and insure the AI economy so companies reap the rewards of this fantastic technology. We are also users of AI, applying it deeply into our business, and our exploring ai assisted underwriting, distribution strategies and broad based automation. More on that, another time!

It’s going to be an absolute privilege underwriting these AI exposures in the home of insurance innovation, Lloyd’s. We will keep you all up to date as we embark on our mission.

Next steps:

Yes. Testudo's standalone Gen AI liability insurance is purpose-built to respond to third-party claims arising from the outputs of generative AI systems deployed by US enterprises. Written on Lloyd's of London paper rated A+ (Superior) by AM Best, it covers financial loss from negligent misrepresentation, IP infringement, defamation, unauthorized data disclosure, and physical harm. Brokers can obtain a quote without a technical audit of the AI system.

Generative AI lawsuits increased 137% in 2025 according to Testudo's litigation data, as more enterprises deployed AI systems that caused third-party harm. These claims are now working through insurers' balance sheets, accelerating the move toward CGL exclusions. Read our Generative AI Litigation Overview for the full data, or see our Q1 2026 market update for what this means for vendor liability.

Mark Titmarsh

Head of Insurance | Co-Founder

Insurance and risk strategist with 15+ years shaping how the industry underwrites emerging technology. A specialist in generative AI, digital asset custody, financial lines, and product innovation, with a track record of building first-of-their-kind offerings for firms including Superscript, Malca-Amit, and Aviva. Known for turning complex, frontier risks into insurable, market-ready products.